The Malaysian Accounting Standards Board (“MASB”) issued the amendments to MFRS 137 Provision, Contingent Liabilities and Contingent Assets. The amendments to MFRS 137 is specifically to address the determination of the cost of fulfilling a contract. The determination of the cost of fulfilling a contract is important in order to assess whether the contract is onerous. The amendments is effective for financial period beginning on or after on 1 January 2022. Entities however, can early apply the amendments before its effective date.

Let us now understand what are the amendments and how they affect you.

What are onerous contracts?

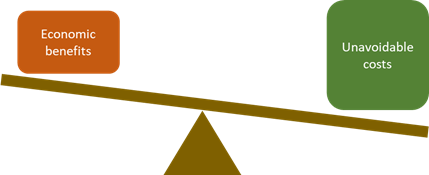

First, what is onerous contract? MFRS 137 defines an onerous contract as “a contract in which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it.”

When a contract is an onerous contract, paragraph 66 of MFRS 137 requires entities to measure and recognise a provision for such a contract. A provision is a liability of uncertain timing and amount.

The logic to recognise a provision is because an entity has a present obligation to incur such cost/provision amount to fulfil its obligation under such a contract.

What if the contract is not onerous? In such a situation, entities will not a provision in their financial statements. Contracts that are not onerous fall outside the scope of MFRS 137. Accordingly entities apply other standards, such as MFRS 15 Revenue from Contracts with Customers. Thus, it is critical to assess whether a contract is an onerous contract or not.

Challenges in determining onerous contracts

We understand earlier that unavoidable costs is one of the elements in assessing onerous contracts. Assessing unavoidable cost itself requires significant judgment by entities.

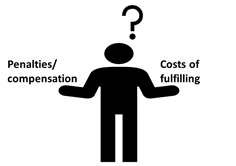

But what is ‘unavoidable costs’? MFRS 137 currently explains that unavoidable costs under a contract reflects the least net cost of exiting from the contract. The cost of exiting from a contract could either be:

- the penalty or compensation that an entity has to pay to the contracting party upon failing to fulfil its obligation

- total costs to be incurred in fulfilling the obligation under the contract.

Accordingly, the lower of the two amounts is the unavoidable costs.

Most of the time, contracts will state the expected penalties or compensation that an entity has to pay upon failing to fulfil its obligation. Hence, entities can easily determine the amount

The challenge and mixed practices observed, however, is in relation to determining the cost of fulfilling such an obligation. Generally, there are two types of costs entities consider in determining the cost of fulfilling:

- Incremental costs that entities expect to incur in fulfilling the contract. Examples are direct labour and materials.

- Other costs, such as allocation of other general costs that relate directly to fulfilling the contract, such as allocation of depreciation for property, plant and equipment used for the contract.

Determining the cost of fulfilling the obligation

Currently, some entities only consider the incremental costs in determining the costs to fulfilling the obligation. Some other entities, on the other hand, take the full costs approach to determine the cost of fulfilling. Under the full costs approach, entities take into account the incremental costs and other costs. Accordingly, there are divergence in practice among the companies.

The amendments to MFRS 137 aim to promote consistent application of accounting standards and consistent practice. The amendments clearly state that an entity must consider both – incremental costs and other costs – in determining the cost of fulfilling a contract. Accordingly, an entity applies full costs approach when the amendments become effective.

What are the rational of full costs approach? The basis for the selection of the full cost approach is because:

- Firstly, the inclusion of all costs provides more useful information to the users of the financial statements.

- Secondly, the benefits of providing such information are likely to outweigh the cost required to obtain such information.

- Lastly, the inclusion of all costs that relate directly to the contract regardless of whether it is an incremental cost or other cost is consistent with other requirements in MFRS 137 and other standards.

The amendments give an impact to entities which are currently adopting the incremental cost approach as its accounting policy. With the amendments, we also expect more contracts to be onerous contracts due to the full costs approach. This is as the consequence of more costs will be included in determining the cost of fulfilling a contract.

The impact to entities

Under the transitional provision, an entity is required to apply the amendments to its contracts for which it has not yet fulfilled all its obligations at the date of initial application. However, entities do not need to restate the comparative numbers. Instead, entities recognise the adjustments upon applying the amendments to the opening balance of retained earnings or other components of equity at the date of initial application.

Similar to the adoption of other amendments, we suggest you to start the assessment early to determine the impact of the amendments to your financial statements. The full set of amendments is available at Onerous Contracts—Cost of Fulfilling a Contract (Amendments to MFRS 137) on the MASB website.